Executive Summary

For decades, development site values in New York City have been driven by three primary variables: zoning, market conditions, and location. Today, a fourth variable has emerged as equally powerful—political alignment. What has changed is not just the importance of politics, but where we are in the cycle. The 2025 New York City Council elections have already occurred, and the market has moved from uncertainty to interpretation.

That shift matters. Prior to the election, buyers priced risk conservatively because they did not know what the policy environment would look like. Today, the composition of the Council taking office in 2026 is known, and capital is recalibrating in real time. The market is no longer asking what might happen, it is asking what the results mean, how elected officials are likely to behave, and how quickly those behaviors will translate into approvals, delays, or denials.

For owners of development sites, this is a moment of opportunity. The market has more clarity than it did six months ago, but pricing has not yet fully adjusted to the new reality. That gap, between understanding and full repricing, is where strategic decisions can create meaningful value.

I. From Uncertainty to Interpretation

In the months leading up to the election, the development market slowed—not because capital disappeared, but because conviction did. Developers hesitated, underwriting became more conservative, and many transactions were deferred. The issue was simple: no one knew what the next Council would look like or how it would approach development.

That uncertainty has now been removed and activity in the market has picked up considerably.

The election results have established the legislative body that will shape land use decisions for the next four years. While policy outcomes will take time to fully materialize, the market does not wait for legislation. It responds immediately to perceived direction. As a result, we are now in a transitional phase where buyers are actively re-underwriting opportunities based on the expected behavior of newly elected officials.

This is the most important insight for owners: the market has clarity, but not yet consensus. Pricing is beginning to move, but it has not fully reset. That creates a window and that window is one that historically has been short-lived.

II. What the Election Results Signal

The most critical question is not who won individual races, but what the collective composition of the Council suggests about the direction of policy. From a market perspective, three themes are emerging.

First, the environment is increasingly negotiation-driven. The Council is not uniformly aligned in either direction. Instead, development outcomes will depend on how well projects are positioned within policy priorities—particularly around housing production, affordability, and community impact. This is not a market where projects move forward automatically, but it is also not one where development is broadly constrained. It is a market where alignment must be demonstrated.

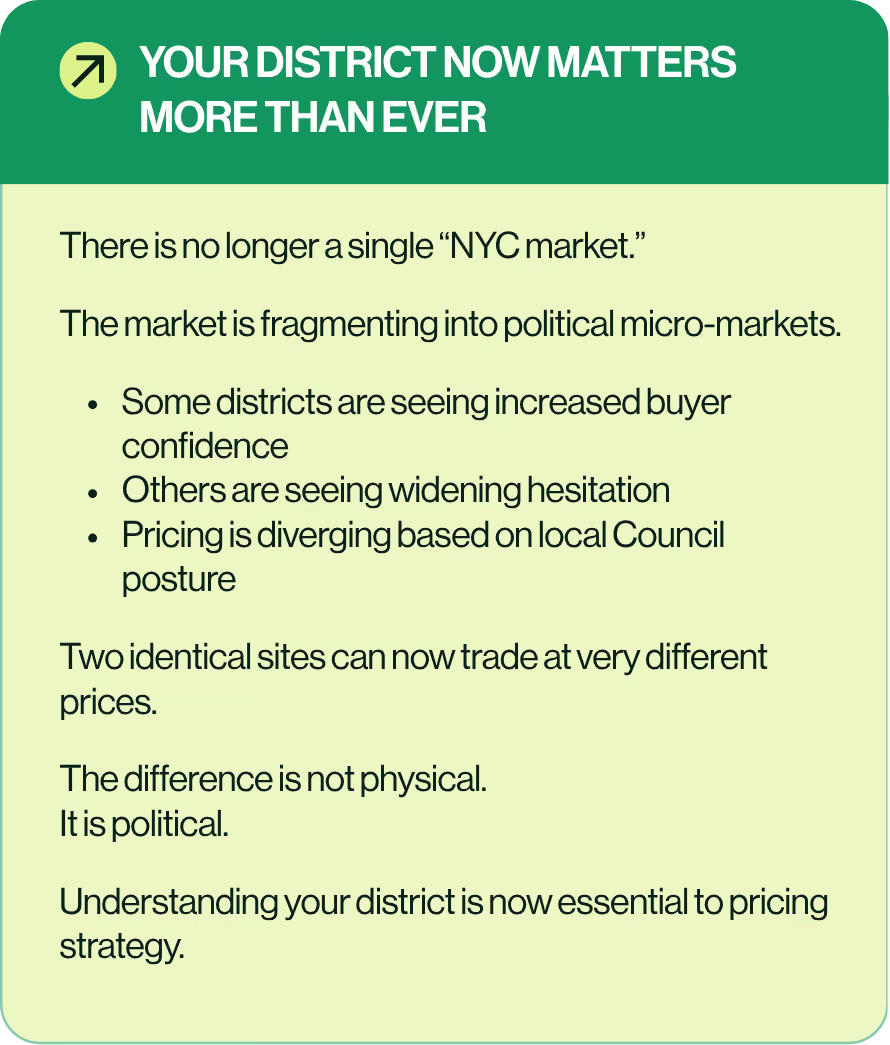

Second, district-level variation is becoming more pronounced. The idea of a single “New York City market” is becoming less relevant. Instead, the city is fragmenting into micro-markets defined by political posture. In some districts, the path to approval is becoming clearer and more predictable. In others, it is becoming more complex and uncertain. This divergence is already being reflected in how buyers evaluate opportunities. For example, at BKREA we are now doing something that we have never done before taking the political leanings of the local council member into our Broker Opinions of Value.

Third, leadership matters more than ever. The tone set by Council leadership—particularly around housing, conversions, and rezonings—will influence not just individual approvals, but the consistency of the process itself. For capital, consistency is as important as policy direction.

III. District-Level Signals: Where the Market Is Repricing

While the overall composition of the Council provides direction, the market ultimately prices development sites at the district level. Certain races carry disproportionate weight because of their location, their development potential, and their historical posture toward growth.

Manhattan District 4 (Midtown East)

With the election of Keith Powers’s successor, the market is closely analyzing how Midtown East will be approached going forward. This district sits at the center of the city’s commercial core and contains some of the most significant office conversion and redevelopment opportunities in New York. Early interpretation suggests a pragmatic, structured approach to development, which is beginning to restore confidence among buyers. Even modest improvements in approval predictability here can have an outsized impact on land values given the scale of opportunity.

Bronx District 17

The transition from Rafael Salamanca Jr.—widely viewed as one of the more constructive voices on development—to new leadership is one of the most closely watched shifts in the city. The Bronx has been an area where development has been relatively feasible, and the degree to which that continues will directly influence capital flows into the borough. Early signals suggest cautious continuity, but the market is still in the process of forming conviction.

Brooklyn District 33

In Brooklyn, Lincoln Restler’s district remains one of the most actively scrutinized development environments. The policy posture here is best described as engagement with conditions—projects can move forward, but they must be carefully structured. For buyers, this translates into a need for precision in underwriting and positioning. For sellers, it reinforces the importance of narrative and alignment.

Manhattan District 1

Lower Manhattan, represented by Christopher Marte, continues to present a complex but evolving environment. With significant office-to-residential conversion potential, the district sits at the intersection of policy ambition and practical feasibility. The market is watching closely to determine whether conversion activity will be enabled at scale or constrained by process.

IV. The Evolution of the Political Discount

Prior to the election, the market applied a broad-based political discount across development sites. In the absence of clarity, buyers assumed risk conservatively, often widening their required returns to account for unknown outcomes.

Today, that discount is being recalibrated—but not uniformly.

In districts where the election results suggest a more predictable and pragmatic approach to development, the discount is beginning to compress. Buyer confidence is increasing, bidding is strengthening, and pricing is moving upward. In districts where policy direction appears more restrictive or uncertain, the discount is widening, reducing competition and placing downward pressure on values.

This divergence is one of the defining characteristics of the current market. It means that two sites with identical zoning and physical attributes can now trade at materially different prices based solely on political context. For owners, this makes district-level understanding essential.

V. Policy Implications: What Happens Next

While elections provide direction, policy execution will determine outcomes. The next phase will be defined by how the new Council translates its composition into action.

Rezonings remain the most powerful driver of land value.

Even incremental increases in allowable density can create significant value, while resistance can suppress it. The market will be watching closely to see where the Council is willing to support increased density and where it is not.

Office-to-residential conversions represent another critical opportunity. With structural challenges in the office market, conversions offer a logical path to increasing housing supply. The key question is whether policy will evolve to make these projects economically viable at scale. Early signals are constructive, but execution will depend on specifics.The 467M tax abatement program has been very compelling and the private sector has been taking full advantage of it.

Finally, development economics will continue to be shaped by regulatory layering. Affordability requirements, labor considerations, and other policy elements all impact feasibility. The cumulative effect of these factors can determine whether a project proceeds or not, and therefore directly influences land value.

VI. How Capital Is Responding

Capital is already reacting to the new environment. In the immediate aftermath of the election, we are seeing a selective re-engagement from developers who had previously been on the sidelines. However, this re-engagement is not uniform.

Developers are targeting districts where political alignment appears favorable or at least manageable. In these areas, competition is increasing and pricing is strengthening. In less aligned districts, capital remains cautious, and in some cases, absent.

This selective deployment of capital is widening the gap between districts. For sellers, this gap represents a critical variable in determining both timing and strategy.

VII. Strategic Implications for Development Site Owners

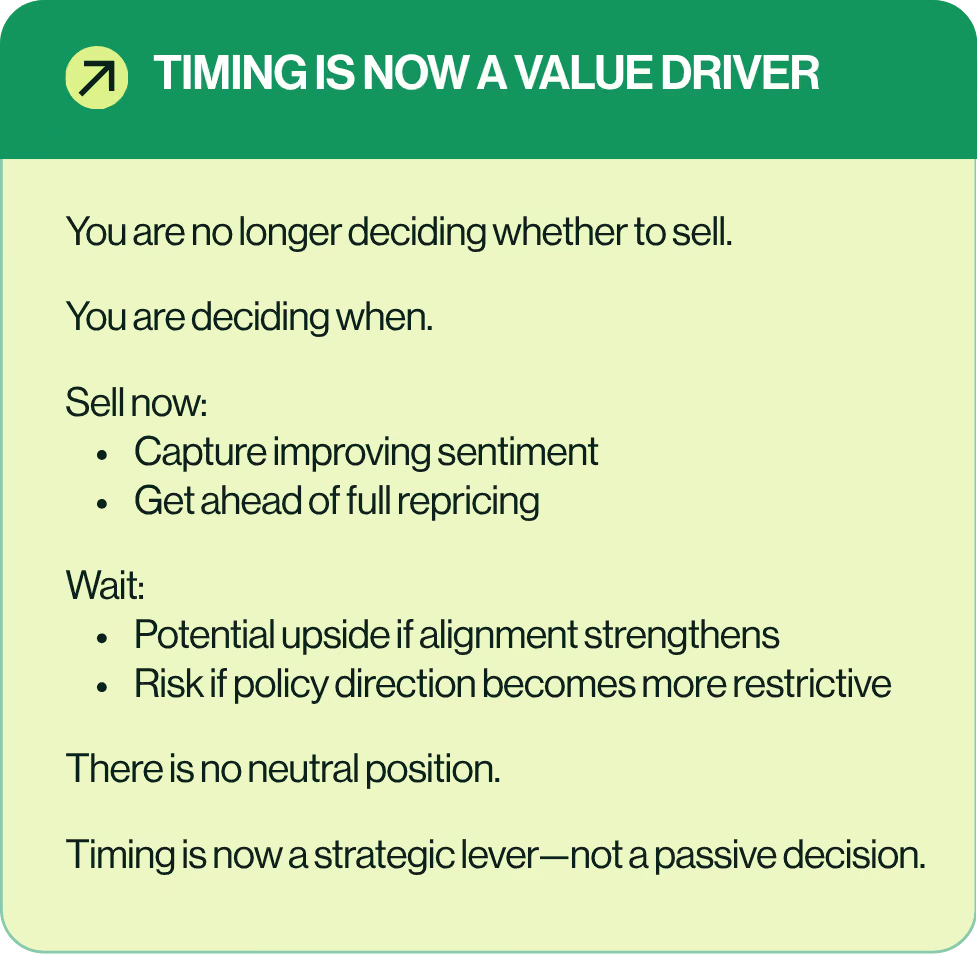

For owners, the current moment presents a unique opportunity—but one that requires decisiveness.

First, there is an opportunity to sell into a window of partial clarity. Buyers have more confidence than they did pre-election, but pricing has not yet fully adjusted. This creates a favorable environment for sellers who act before the market fully resets.

Second, waiting for complete policy clarity is often counterproductive. By the time policy direction is fully established, pricing will have already adjusted. The optimal window is typically before consensus forms.

Third, positioning matters more than ever. Development sites must be framed within the context of the current policy environment. Aligning with priorities such as housing production, adaptive reuse, and community benefits can materially impact buyer interest and pricing.

Finally, targeting the right buyers is critical. Different developers will interpret the new environment differently. Identifying those whose strategies align with the emerging policy landscape is essential to maximizing value.

VIII. The Broader Context: Supply and Market Direction

At its core, the implications of the election results extend beyond individual transactions. They will shape the trajectory of housing supply in New York City. The city’s housing challenges are driven by structural undersupply, and increasing production remains the most direct path to addressing that imbalance.

The composition of the new Council suggests that development will continue, but it will require alignment, negotiation, and strategic execution. This is not a market defined by automatic approvals, but by deliberate outcomes.

Conclusion: A Market in Transition

The New York City development market has entered a new phase. The uncertainty that defined the pre-election period has been replaced by interpretation, recalibration, and selective re-engagement. For owners of development sites, this is a moment that demands clarity of thought and decisive action. The market is moving, but it has not yet fully repriced. That creates a window—one that will not remain open indefinitely. The BKREA land team is happy to advise you on the development leanings of your local council person.

The rules of value have evolved. Zoning still matters. Location still matters. Market conditions still matter. But increasingly, value is being shaped by something more nuanced and more powerful: the alignment between development and policy. This is particularly true for sites that are not completely as-of-right.

And in today’s market, that alignment is what determines whether a site achieves its full potential—or falls short of it.

Bob Knakal | Chairman & CEO

bk@bkrea.com | 917.509.9501

Bob Knakal has been a broker in NYC since 1984. Over that time, he has brokered the sale of over 2,422 buildings having a market value of approximately $24.8 billion. The 2,422 properties sold Is generally considered to be the highest total for any individual broker in the history of the United States.

For 26 years of those years (1988-2014), he owned and ran Massey Knakal Realty Services which sold more than 3x the number of properties as the #2 firm in NYC from 2001-2014. Running the firm with a Servant Leadership management style, focusing on empowering everyone on the team, intensely training them and building their self-esteem, led to this overwhelmingly dominant platform. The firm was sold to Cushman & Wakefield in 2014 for $100 million.

The Massey Knakal Legacy is illustrated by the fact that today in the New York City investment sales market, there are 35 companies, or divisions of companies, that are either owned by, or run by, folks who learned the business at Massey Knakal.

Bob is a prominent thought leader in the commercial real estate business, frequently writing about the market, lecturing on the market, and appearing on podcasts and national television shows on networks like Fox, CNBC and MSNBC.